Starting Your Medicare Journey

Turing 65 in the USA marks a big milestone in the USA. Typically, this is the first time someone will be eligible to enroll into the Federal Health Insurance Plan for Americans 65 or older which we call Medicare. While there are many situations where someone younger than 65 could have Medicare, this article will focus on people 65 years old or older.

This article will provide you with a fundamental understanding of what Medicare is. We will be covering the following topics:

Contents

What is Medicare

Who can Get Medicare

How to Enroll in Medicare

Timelines

The different types of plans that work with Medicare.

What is Medicare

So, what is Medicare? Medicare is the Federal Health Insurance Program for people age 65 or older. The program helps cover the cost of healthcare, but it does not cover all your medical expenses.

Original Medicare consists of two parts: Part A & Part B.

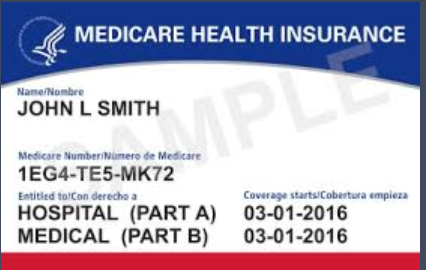

Standard Medicare Health Insurance Card

Medicare Part A (hospital insurance) helps cover inpatient care in hospitals (including critical access hospitals) and skilled nursing facilities (not custodial or long-term care).

Medicare Part B (medical insurance) helps cover medically necessary doctors’ services, outpatient care, home health services, durable medical equipment, mental health services, limited outpatient prescription drugs, and other medical services. Part B also covers many preventative services.

Parts C & D

Part C, also known as Medicare Advantage, is a way for Medicare beneficiaries to receive their Medicare Benefits. This is a way to receive your Part A, B, & D benefits in one single plan. These plans are administered by private companies who have contracts with the Centers of Medicare. There are many types of plans but the important thing to understand is once you enroll into a Medicare Advantage plan you will have to receive all your benefits through the plan. The main highlights of these plans are their Maximum Out-of- Pocket limits that cap your costs for healthcare and their extra benefits like dental and vision.

Part D, also known as Prescription Drug Plans, are the plans that cover the cost of medication. These plans are administered by private companies who have contracts with the Centers of Medicare. Original Medicare does not cover medications. While Medicare states that joining a Part D plan is voluntary if you have more than a 63-day break without coverage there is a late enrollment penalty. Part D plans typically have a monthly premium, deductible, co-payments or co-insurance and formularies (list of covered medications).

Who can Get Medicare

Medicare Part A (hospital insurance) People age 65 or older, who are citizens or permanent residents of the United States, are eligible for Medicare Part A. You’re eligible for Part A at no cost at age 65 if one of the following applies:

• You receive or are eligible to receive benefits from Social Security or the Railroad Retirement Board (RRB)

• Your spouse (living or deceased, including a divorced spouse) receives or is eligible to receive Social Security or RRB benefits

• You or your spouse worked long enough in a government job through which you paid Medicare taxes. You or your spouse need 40 credits or about 10 years of working and paying FICA taxes.

Medicare Part B (medical insurance)

Anyone who’s eligible for Medicare Part A at no cost can enroll in Medicare Part B by paying a monthly premium. Some people with higher incomes will pay a higher monthly Part B premium.

Medicare Part C (medical insurance & drug coverage)

Must have Part A & Part B, live in the service area, be a US citizen or lawfully present in the U.S.

Medicare Part D (prescription drug insurance)

Anyone who has Original Medicare (Part A or Part B) is eligible for Medicare prescription drug coverage (Part D).

How to Enroll in Medicare

Auto Enrollment if you are Receiving Social Security Benefits

Some People Get Part A and Part B Automatically If you’re already getting benefits from Social Security or the RRB, you’ll automatically be enrolled in both Part A and Part B starting the first day of the month you turn 65. If your birthday is on the first day of the month, Part A and Part B will start the first day of the prior month.

If You are not Receiving Social Security Benefits

If you’re approaching age 65 and not receiving benefits, you should contact the Social Security Administration about three months before your 65th birthday to sign up for Medicare. You can use their website https://www.ssa.gov/ , go in person to your local office, or call 1 (800) 772 – 1213.

Timelines

Enrolling in Medicare

Best practice if you are not receiving Social Security Benefits is to contact the Social Security Administration 3 months before your 65th birthday. If you receive Social Security benefits, then you will be automatically enrolled.

Initial Enrollment Period

(new to Medicare)

Starts 3 months before you get Medicare (Part A and/or Part B) and ends 3 months after you get Medicare.

Medigap Open Enrollment

You get a 6 month “Medigap Open Enrollment” period, which starts the first month you have Medicare Part B and you’re 65 or older. During this time, you can enroll in any Medigap policy and the insurance company can’t deny you coverage due to pre-existing health problems. After this period, you may not be able to buy a Medigap policy, or it may cost more. Your Medigap Open Enrollment Period is a one-time enrollment. It doesn’t repeat every year, like the Medicare Open Enrollment Period

Open Enrollment Period

October 15-December 7.

Join, drop, or switch to another Medicare Advantage Plan with or without drug coverage (or add or drop drug coverage).

Switch from Original Medicare to a Medicare Advantage Plan or from a Medicare Advantage Plan to Original Medicare.

Join, drop, or switch to another Medicare drug plan if you’re in Original Medicare.

Medicare Advantage Open Enrollment Period

(only if you’re already in a Medicare Advantage Plan)

January 1-March 31.

The different types of plans that work with Medicare

Medicare Advantage Plan

Plans that cover Part A, B, & D benefits along with additional benefits like dental, vision, and over the counter allowances. When you join one of these plans you agree to receive your Medicare benefits through the plan. There are several different types of Medicare Advantage plans HMOs, PPOs, and Special Needs Plans. Regardless of what type of plan you choose, keep these things in mind:

• You can only be in one Medicare Advantage Plan at a time.

• You can join a plan even if you have a pre-existing condition.

• You must use the card from your Medicare Advantage Plan to get your Medicare-covered services. Keep your red, white, and blue Medicare card in a safe place because you may need it for some services, or if you ever switch back to Original Medicare.

• In many cases, you’ll need to use health care providers in the plan’s network. When an in-network provider or benefit isn’t available or can’t meet your medical needs, most plans will help you get any medical care outside the provider network (at the in-network cost sharing).

Prescription Drug Plan

Medicare drug coverage (also known as Medicare Part D) helps pay for the brand-name and generic drugs you need. It's optional and offered to everyone with Medicare by insurance companies and other private companies approved by Medicare. Even if you don’t take prescription drugs now, consider getting Medicare drug coverage to avoid paying a late enrollment penalty if you join a plan later.

Medicare Supplement/ Medigap

Medicare Supplement Insurance (Medigap) is extra insurance you can buy from a private insurance company to help pay your share of out-of-pocket costs in Original Medicare, like copayments, coinsurance, and deductibles

You can only buy Medigap if you have Original Medicare. Generally, that means you have to sign up for Medicare Part A (Hospital Insurance) and Part B (Medical Insurance) before you can buy a Medigap policy.

All Medigap policies are standardized. This means, policies with the same letter offer the same basic benefits no matter where you live or which insurance company you buy the policy from. There are 10 different types of Medigap plans offered in most states, which are named by letters: A-D, F, G, and K-N. Price is the only difference between plans with the same letter that are sold by different insurance companies

Sources:

https://www.medicare.gov/basic